The cold reality coming off a hot summer is that as reported in The Street.com, capital raising in the U.S. cannabis industry is down 67% this year. Viridian reports that through June there were 166 capital raises for $2.6 billion as opposed to 230 deals for $5.5 billion for the same period in 2019. In 2020, 32 companies raised capital in the first half. In 2019, 109 were funded during that same period. The Future of Cannabis Investing

Coming off the dramatic decline of Canadian cannabis pubco stocks in 2019, it is little wonder that this sharp decline in fundraising and in M&A activity has characterized this year. Winners in the midst of the decline were real estate SPACs ad REITS offering sales-and-leaseback transactions as cannabis grew into a maturing industry where companies with accumulated assets could now access debt financing. Hemp capital was also off by 78% during this period of oversupply with dropping CBD prices accompanied by numerous chapter 11 filings. The Future of Cannabis Investing

During the first half it is interesting to note that the biotech industry enjoyed a 92.3% increase in capital raises. More about that later in this report.

While the experience in 2019 demonstrated the folly of overreach and speculative enthusiasm, the benefit has been the market maturation going on in 2020 – a period where not only fundamentals are dominating, but also where the future of the cannabis industry is becoming more and more apparent. The Future of Cannabis Investing

What is the Path Toward the Future?

The Future of Cannabis Investing

Sources like Grand View Research continue to report that the global legal cannabis market is still headed toward being worth $73.6 billion by 2027. This is based on the fact that global sales will grow as more U.S. states and countries around the world legalize medical and recreational cannabis. Vital to promoting this growth will be the necessary movement by Big Finance to take the lid off the cash constraints the cannabis industry faces. All eyes will be turning toward the SAFE Banking Act in the coming months. Insight into the path the cannabis industry is taking toward a lucrative future is that medical marijuana accounted for 71% of total legal sales in 2019. Granted only 14 of the 33 legal states and the District of Columbia allow recreational marijuana sales. Nevertheless, the disproportionate share of medical marijuana sales is indicative of the aging population demographic in the U.S. that is shunning opioids taken for chronic pain relief and turning to cannabis. The Future of Cannabis Investing

CBD

The marijuana plant contains active ingredients called cannabinoids. The first and second most abundant of these are tetrahydrocannabinol (THC) and the popular cannabidiol (CBD). CBD has certainly become an overnight success story in the area of self-prescribed medical treatment. It has attracted large scale investment from global companies such as Constellation Brands (NYSE:STZ.B) and Altria Group (NYSE:MO). Projected to reach a market size as large as $22 billion by 2022, according to the Brightfield Group, CBD is still a cannabis product category beset with regulatory problems. Fits and starts are characteristic of the marketing efforts of CBD companies to date due to the vagaries of the laws in state and local jurisdictions. Consequently, none of the companies attempting to establish national brands have risen to level of market leadership. Yet, predictions are still strong that these hurtles will be overcome and consumer demand will pull this facet of the cannabis industry to its full potential.

Active Pharmaceutical Ingredients (APIs)

THC and CBD are just two of the approximate 144+ cannabinoids that can appear in trace amounts in a marijuana plant. Many of these cannabinoids are soon to be making their way as Active Pharmaceutical Ingredients (APIs) in pharmaceutical medications for the treatment of chronic pain, glaucoma, epilepsy, and the growing body of research in the treatment of HIV/AIDS, Lupus, and MS. Along with this are promising developments with anti-proliferative effect on different types of cancer cells. And, cannabinoids as APIs are also being introduced into medications that hold the promise of reducing the dosages of opioids and prompting the discovery of treatments for Alzheimer’s Disease.

In the early 1990’s the endocannabinoid system in the human body was discovered that controls critical biological functions such as pain, memory, sleep and immune functions. Since then pharmaceutical manufacturers and research facilities have been attempting to work around the policies of government restrictions to be able to conduct meaningful research on the effects of various cannabinoids when they bind to receptors in this internal human endocannabinoid system. Most recently, however, with the popularity of cannabis legalization growing around the world and with the lure of lucrative legal markets that have emerged, governments are fast-tracking the legalization processes relating to pharmaceutical-grade cannabis production and R&D.

Three years ago the U.S. FDA approved GW Pharmaceuticals’ drug Epidiolex for the treatment of a rare and severe form of childhood epilepsy called Dravet Syndrome. That landmark decision marked the first time a medication that contains a cannabinoid derived from marijuana was approved by a US federal agency. That has prompted other major players in the pharmaceutical industry to look for ways to develop cannabinoid-derived medicines, as well as safe and effective consumer products.

- GW Pharmaceuticals has also developed Sativex, from extracts of THC and CBD for sale in countries that allow it for treatment of spasticity and has intensified development programs in ophthalmics, cystitis, fibromyalgia and opioid reduction.

- Nexien BioPharma has one granted patent and seven patents pending.

- In the UK, Brains Bioceutical, a global leader in EU cGMP production of plant-based cannabidiol as an API for pharmaceutical and nutraceutical use, recently secured a $30M capital infusion to continue its clinical testing. This includes a phase III clinical trial for an adult epilepsy drug and expands by sevenfold the production of its CBD API in order to meet demand.

- And, opening the door to more extensive R&D, the World Health Organization Expert Committee on Drug Dependence recommended to the United Nations commission on Narcotic Drugs that cannabis-based preparations proven to be pure Cannabidiol (CBD) should be rescheduled under all international drug control treaties.

The global Cannabinoid drugs market is segmented into the following regions: North America, Latin America, Western Europe, Eastern Europe, Asia-Pacific Excluding China & Japan, China, Japan and the Middle East and Africa. North America is dominant in the global cannabinoid drugs market mainly due to the high presence of top players and huge investments being made for cannabinoid drugs development. In North America, particularly the USA holds a dominant position. Economic conditions in the APAC region are set to drive the cannabinoid drugs market to new heights. The European cannabinoid drugs market is the fastest growing market due to a changing legislative climate. Growth in the Middle East and African region is expected to be considerably less when compared to the other regions. However, developed economies, such as Australia, will witness highest growth rate in the cannabinoid drugs market.

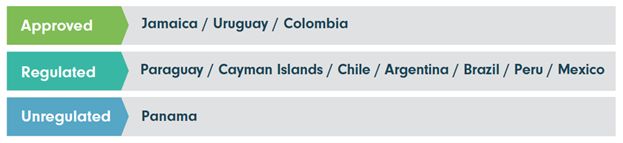

Comprised of 42 countries, 650 million people, 10 LATAM countries have legalized cannabis for medicinal use, 3 have decriminalized it for adult use. Over 40 licensed producers throughout the region enjoy the competitive advantages of prime real estate with ideal growing conditions,

exceptional climate appellations, sunshine and water resources. Among the advantages, though, the overarching factor is the price of labor. It is estimated by Green Fund that the LATAM potential to produce cannabis in commercial quantities will be nearly 80% less than the rest of the world.

The LATAM Regulated Market

Nevertheless, LATAM brings its share of concerns about instability and unrest that are potential red flags for investors. Among the opportunities throughout the region, however, we find one country stands out as offering the most exciting potential for short-term growth and long-term stability.

It is questionable if any other country has ever been associated with cannabis the way Jamaica has been viewed throughout the world. Deep roots in cannabis stretch back for over 100 years, with Bob Marley becoming Jamaica’s most notable international icon. Jamaica was one of the first LATAM countries to decriminalize cannabis – as early as 2015. In 2015 came the establishment of Jamaica’s Cannabis Licensing Authority (CLA) that began the regulation and licensing of legal cannabis businesses in the country. International cannabis commerce for Jamaica began in 2018 with the first shipment of medical-grade extract to Canada.

Investors and companies eager to do business with Jamaica have been awaiting final import/export legislation by the CLA. The government is taking the tack that its actions are carefully structured to strengthen the cannabis industry for the benefit of Jamaica and its trading partners.

Future of the Largest Market for Cannabis

From these developments you can see why pharmaceutical grade cannabis is the future of the modern cannabis industry. In our view it is the key to making smart investments in the category. According to the GMP compliance consultancy PharmOut in their Industry Growth Predictions for 2020- 2025 the global demand for cannabis, medical and recreational, is increasing consistently at a growth rate of 17% to 23% per annum. And, while true medical-grade cannabis will be influenced by supply/demand and cost pressures as well as by stringent cultivation, processing and export regulations, it is not unreasonable as some analysts predict for the global medicinal cannabis market to eventually reach $650 billion – making it the third largest worldwide market after oil and arms.

Driving the Pharmaceutical Cannabis Market

These are the primary drivers boosting the burgeoning growth of the cannabinoid-based pharmaceutical drug market.

- The surge in the number of physicians authorizing medical cannabis because of increasing clinical and empirical evidence and the growing number of patients looking for more natural alternatives to traditional drugs.

- Baby Boomers and Millennials with more liberal attitudes toward cannabis and the experimentation with various forms of alternative remedies.

- Rising tide of opioid abuse requiring an effective replacement medication for the treatment of chronic pain.

- Continuing legislation changes across the globe spurring cannabis demand in its various forms.

- The rapid advancement of technologies that has led to:

- The ability to discover and extract rare cannabinoids from marijuana plants

- Progress in the creation and production of cannabis drug discoveries

Mitigating Risk and Maximizing Upside in this Investment Space

The evidence continues to mount that pharmaceutical cannabis is the future of investing in the industry, however many cannabis companies claim to be “medical cannabis” companies, often making it difficult for investors to tell the real players from the pretenders. Here is the approach we take with our clients for risk mitigation prior to presenting cannabis investment opportunities:

- First, we ascertain if the company and founders have backgrounds in pharmaceutical or cannabinoid-based science. Without this background the chances of success are greatly diminished.

- Second, we ensure that the company is familiar with and focused on meeting EU cGMP requirements for pharmaceutical grade APIs. If they are not, we move on because the lower quality “medical grade” companies are a dime a dozen, and destined for commoditization.

- Third, we assess the regulatory regime in the company’s home market, and in the target markets. And, we analyze the ability of the company to scale in context of near, medium and long-term market expansion as new major international markets come online. In our opinion it is critical for a properly positioned pharmaceutical cannabis company to have the ability to scale rapidly in order to capitalize on the massive global market potential.

Investor Takeaways

While biotech and pharma capital raises are soaring, cannabis funding is down dramatically in the tumultuous year 2020 has been. Nevertheless, global market size projections remain fixed on the cannabis industry being worth $73.6 billion by 2027. And, in relation to biotech and pharma, the lucrative future of cannabis is for medical use – a global medicinal cannabis market that could eventually grow to become the third largest worldwide market after oil and arms. Critical to a decision as to where to invest is the assessment of the regulations in a company’s home country and the target markets it intends to/is capable of addressing. The Future of Cannabis Investing

How We Can Help

While the market growth potential of the future of the medicinal cannabis industry brings with it the upside of fresh startups and growing employment opportunities, careful investigation and specialized knowledge is required for investor and consumer protection. At Highway 33 Capital Advisory we are standing by with the expertise and experience to provide guidance. We excel at structuring deals to meet client investment strategies in trending segments like cannabis pharmaceutical grade APIs as well as our core expertise with highly regulated markets in the fields of pharma, biotech, healthcare, Agtech, and CBD/hemp companies as well as technology companies. We specialize in thoroughly vetted companies that are looking to drive growth and enterprise valuations through M&A, non-dilutive debt financing and/or capital investments ranging from $5M to $100M+.

Let’s talk about putting the power of this expertise to work for you as a Sell or Buy-side client.