Disparity in Access to Capital Raising Capital in the Cannabis Industry 2021

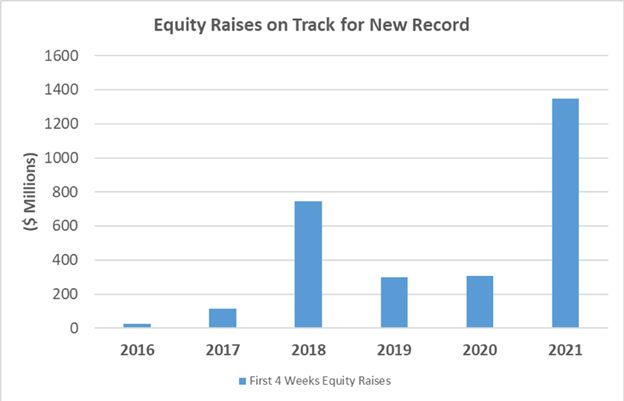

Through May, capital raised in the cannabis industry totaled over $6.6 billion, compared to only a little over $2.3 billion in 2020. With growing consolidation in the industry Mergers & Acquisitions, which recorded over $600 million in transactions in Q4 2020, are already exceeding last year’s record. And as more debt providers come online, recent multimillion-dollar debt funding among cannabis industry leaders shows that debt as a capital source for cannabis companies is a rational use of capital. Raising Capital in the Cannabis Industry 2021

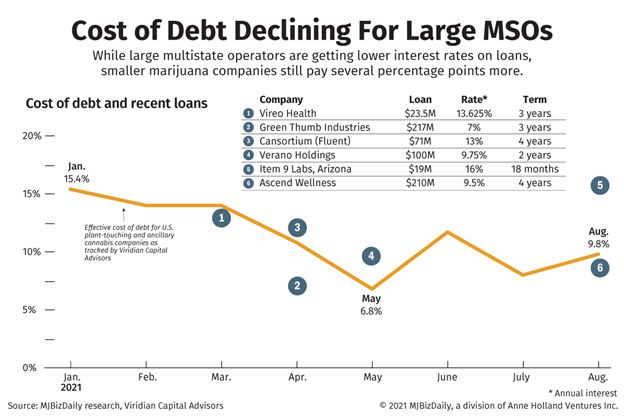

However, Marijuana Business Daily reports that large cannabis MSOs that have strengthened their balance sheets now qualify for lower loan interest rates these days. On the other hand, smaller MSOs, typically receive annual interest rates of about 13%, according to an MJBizDaily examination of recent debt deals. The legal firm Reed Smith also reported on the cost of this same capital being still fairly high for smaller operators. The lower debt costs highlight the interest-rate gap between large operators and smaller businesses, including minority-owned companies. Raising Capital in the Cannabis Industry 2021

About this disparity,The Chicago Tribune says:

…newly licensed vertical integrated cannabis operator anxious about it, because now the hard part starts for license holders — hustling for funding. Like contestants on the TV show “Shark Tank,” they must sell themselves and their plans to get the millions of dollars they need to get started.

SEC is Clearing Some Hurdles

As Investopedia sees the problem, legality and regulation will continue to be the overarching problem not only in different states within the U.S., but also in different countries as well. Banking continues to be a challenge, of course. And, in Cannabis Business Times a frustrated dispensary owner points out the root of the problem – the 280E Task Penalty. This restriction on a cannabis business being able to claim business operations expense deductions due to the Federal illegality of marijuana distorts the value of cannabis businesses.

There are, however, cannabis financing alternatives now surfacing for cannabis operators of all sizes including action taken at the end of last year by the SEC that can lighten the burden of limited access to capital. Cannabis Business Executive reports that last November the SEC extended capital raising rules that have strong ramifications for the cannabis industry in a final ruling entitled “Facilitating Capital Formation and Expanding Investment Opportunities by Improving Access to Capital in Private Markets.” With the intent of improving access to capital, these are some of the most important ruling changes pertinent to the cannabis industry: Raising Capital in the Cannabis Industry 2021

- When no money or other consideration is being solicited companies can communicate with potential investors to see how much interest there is and what types of investors are interested without worrying about violating the SEC’s requirements.

- Reg A Tier 2 limit was increased from capping offerings at $50 million to $75 million. This has the potential of accelerating the process for companies now at the upper limit of raising money under this rule.

- The upper limit of unaccredited investors under rule 504 had been increased to $10 million. In the past this restriction in Reg D limited the investment of unaccredited investors to $1 million. That upper limit has now been raised to $10 million.

And in a dramatic change for the SEC, a proposed rule change was announced last year that would allow finders who are helping companies to raise money to receive a commission.

Capital Raising Options

Recent Equity Transactions

Although the majority of the capital flowing into the cannabis industry via the private equity and IPOs has been through large MSOs, this increase in capital is significant for smaller operators for the potential of being acquired. Key equity transactions:

- TerraAscend Corp (CSE:TER)(OTCQB:TRSSF), one of the largest MSOs closed a non-brokered private placement raising C$224 million. The vast majority of this capital coming from what is reported to be four large U.S. institutional investors.

- New York-based, vertically integrated MSO Ascend Wellness Holdings Raised $80 million in an IPO in May. You may recall that Ascend acquired the majority of MedMen’s New York businesses earlier this year.

- In an attempt to begin resolving their long-term liquidity issue Aurora Cannabis (NAS:ACB) last week closed a US$137.9 million public offering with 13.2 million units at US$10.45 per share. This transaction values Aurora at 5.6x its projected 2021 revenue and 61.8x projected 2021 EBITDA.

Capital Creation from M&A Transactions

In March, U.S. News reported that the U.S. cannabis industry had already raised $2 billion in equity capital in 2021. That total was dwarfed on May 10 when in one transaction alone Trulieve acquired Harvest for over $2 billion. Recent major transactions activity:

- In that transaction Trulieve (CSE:TRUL ) (OTC: TCNNF) acquired Harvest Health and Recreation (CSE:HARV , OTCQX: HRVSF) in a $2.1 billion deal that forms in the U.S. what is reported to be the “world’s most profitable multi-state operator.” This is based on the combined adjusted EBITDA of $461 million that Trulieve projects for 2021. Trulieve will now have a retail network of 126 dispensaries across 11 states which they state gives them “an unparalleled platform for continued growth.”

- In January, Canopy Growth announced the filing of an early warning report on maintaining an option for a 20% pro rata ownership interest in TerrAscend. As you have probably watched this mega-deal with us, the final transaction between these two giants is contingent on changes to the Federal regulations on the classification of cannabis in the U.S.

- Following this development TerrAscend closed the acquisition of U.S. companies GuadCo, LLC and KCR Holdings LLC for roughly US$70 million which will expand dispensary operations in Southeastern Pennsylvania.

- Then, In early April came the long-anticipated announcement that Canopy Growth Corp finalized the agreement to acquire Supreme Cannabis Company in a mega-deal valued at US$346 million. Closing is expected this month. Canopy, as you may recall, currently has the largest market cap of all the Canadian cannabis pubcos on the strength of a US$4 billion investment by Constellation Brands.

SPACs in Cannabis

With many VC and PE investors, as well as virtually all institutional investors, staying away from the industry, this puts the use of Special Purpose Acquisition Companies (SPACs) in the limelight – for cannabis companies in the U.S. and in Canada to access capital over traditional sources and in order to pursue the path of going public. In fact, SPACs are bringing substantial liquidity to maintain sales growth and provide cannabis companies with the competitive advantage of more quickly getting to market. In many cases the SPAC merger process with a target company, termed to “de-SPAC,” can take place in a substantially shorter period of time than the traditional IPO timeline. This, though, must be accomplished in a relative short period of time – the two-year requirement for all funds to be invested or, if not, returned to investors. Raising Capital in the Cannabis Industry 2021

Cannabis Industry Maturing to the Point of Turning to Debt

As more debt providers come online, recent multimillion-dollar debt funding among cannabis industry leaders shows that debt as a capital source for cannabis companies is a rational use of capital – potentially cleaning up balance sheets and enabling access to funding for expansion and/or the purchase of distressed assets coming out of the pandemic – to use debt financing for competitive advantage in the marketplace.

While the industry has been capital-constrained, borrowing against assets has been a key source available for many cannabis companies to pursue. Vertically integrated cannabis companies often have significant real estate and other assets that can be leveraged. What has changed now, though, is that more debt providers have come online over the past couple of years addressing a range of needs. This means that cannabis companies can now refinance at more attractive rates. Significant developments: Raising Capital in the Cannabis Industry 2021

- In 2020, large MSOs Curaleaf and Cresco Labs announced their debt raises of approximately $300M and $200M, respectively, illustrating the capital available at the high-end of the market at that time. Then, on January 11 this year, Curaleaf has again secured a new round of financing – a $50 million secured revolving credit facility with a three-year term. Curaleaf will be paying a 10.25% interest rate for funds when needed. This is significantly lower than the interest rates cannabis companies paid for loans in previous years when the likelihood of progress on easing Federal regulations did not look as promising.

- When its stock was floundering in 2020, Acreage Holdings was able to raise debt with the credit arm of an unidentified institutional investor, for up to $100M; as opposed to further diluting equity at their weak stock prices at the time.

- Chicago-based MSO Green Thumb Industries raised $217 million through the issuance of senior secured debt to retire existing senior secured debt and for “growth initiatives.” With an interest rate of 7% per year for the maturity date of April, 2024, Green Thumb describes this transaction as industry leading.

- HEXO Corp. (TSX: HEXO)(NYSE: HEXO) closed a public offering of $360 million principal amount of senior secured convertible notes maturing May 1, 2023. Proceeds will fund the $331 million cash payment in HEXO’s $766 million acquisition of Redecan in Ontario, the largest private Canadian LP.

Debt Financing in Cannabis, What are the Options?

Sale and Leaseback Transactions

- While Sale-Leaseback (SLB) transactions aren’t technically debt they do allow companies to free up liquidity from their balance sheets without dilution. The upside of this alternative is that cannabis companies increasingly have been selling their cultivation, processing and storage facilities and immediately leasing them back as a way to instantly raise tens of millions of dollars. The potential downside is that an SLB locks the asset seller into a long commitment than other straight debt alternatives that now are likely to be able to be secured for rates similar to the SLB. It should be noted, however, that in common debt transactions lenders will be looking for more than a mere promise to repay. A security interest and/or corporate or personal guarantee will most likely be required.

Asset-Based Lending

- Based on the valuation of real estate and equipment assets, a cannabis company can typically borrow from within the range of 40% to 75% of asset value. In the case of development projects, the loan is usually based on project costs. While less typical, there are some working capital debt options in the market as well; though the availability of this option is much less than for real estate and equipment financing.

Convertible Options

- Up to this point, most debt financing by cannabis companies was found in convertible note options with low conversion premiums – which essentially delay dilution of equity. The company creates a note that converts to equity, often preferred stock, at a future date based on a future valuation method. These notes, similar to promissory notes with interest payable on or before a maturity date, have given investors security that they are repaid before equity holders if something goes wrong. For both the investor and the company this note structure allows the valuation question to be answered in the future while providing needed capital to the company and a more secure instrument to investors.

MTN – Short-Term Solution to Minimize Dilution with Funding at Single Digit Rates

- True, that the three alternatives listed above are considered the standard. Now, however, a new alternative is emerging, the Medium Term Note (MTN) for companies with relatively strong balance sheets. An MTN is an alternative to traditional long-term and expensive short-term financing – to aid a company with such objectives as accelerating a growth strategy, facilitating a roll-up M&A strategy.

- An MTN is essentially a bond issuance through investment bankers and funded by private institutional sources, in the range from $20M to $100M+, with specific characteristics to facilitate being issued quickly in order to take advantage of temporary market opportunities.

- The key is to effectively customize the MTN with characteristics most advantageous to the issuer that appeal to the strategy of an investor. This results in rates typically lower than other forms of debt financing. With our network of institutional funding sources for MTNs we provide an overview of the funding need and the upside for investors. Then, we assist the issuer with legal, accounting, underwriting, and rating services in order to begin the preparation of the offering.

For companies seeking debt, the following are key considerations:

- Most cannabis debt providers will require personal guarantees (PGs) from principals. This is always a tough decision for founders and one that carries real risk. Are you willing to PG the debt?

- What assets does the company have? Or is purchasing? Real estate, equipment, accounts receivable, other assets?

- Does the company have existing debt? And how much debt can the company take on while not taking undue risk with cash flow?

For investors who are considering lending to cannabis companies the following are key considerations:

- What are the credit scores of the principals? Is there any credit data on the company? How timely do they pay their payables, for example?

- What is the company’s existing cash flow? How realistic is the projection for future cash flow?

- How will the company use the funds? Is the use of funds realistic?

- What security will the investor have that they can recover funds if the loan isn’t repaid? PG? Cross-corporate guarantee? First lien on assets?

- Does the management team have the right experience for the type of project/company that they want to be?

- Does the company have its state and local cannabis licenses? If real estate is involved, what is the status of current local permits?

The Growth of Funds Dedicated to Cannabis Financing

Also bringing fresh capital to the industry are funds dedicated to supplying financing for equity and debt transactions.

Toward the end of 2020 Intrinsic Capital Partners formed the fund Intrinsic Health Partners, LP, a $102 million growth equity fund formed to invest in life science and technology companies that are focused on the cannabis and hemp industries. To date Intrinsic has provided $65 million in funding for four non-plant touching portfolio companies.

Tysons, Virginia-based Altmore Capital, a senior secured debt lender closed its first cannabis debt fund exceeding its goal of capital available for lending by over 200 per cent. This new fund will be made available to plant-touching operators with more than $10 million in revenue. The fund is projecting the potential of increasing financing to single operators and MSOs by $200 to $300 million in 2022.

The booming marketplace in 2021 is generating renewed interest in cannabis commercial (CRE) investments. Not only are more debt funding options becoming available to cannabis operators, but also how well the cannabis industry performed during the COVID-19 crisis has shown traditional financing sources and formerly reluctant landlords that the cannabis industry exhibits recession-proof qualities. Neglected store fronts in formerly derelict areas and industrial warehouses continue to escalate in value brought on by industry expansion, particularly into areas dedicated as Green Zones within municipalities.

A Green Zone is an area designated where legal cannabis/cannabis-related businesses are allowed/encouraged to set up cultivation, manufacturing and retailing facilities. One funding resource, Canna-Hemp Debt Fund , estimates that industrial warehouses they are underwriting that are “green zoned” show at least a 20 to 30% in increase value. For debt loans the company feels comfortable with LTVs of 60-65% in their green zoned properties. For investor security, and to be able to offer lower than market rates, personal guarantees and cross corporate guarantees, wherever possible, are required from their borrowers.

Investor takeaway

The tide of capital flowing into the industry has risen substantially as investors become more confident in the results of state-by-state legalization and the positive signs for federal legalization progress. Through May, capital raised in the cannabis industry totaled over $6.6 billion, compared to only a little over $2.3 billion in 2020. With growing consolidation in the industry Mergers &. Acquisitions, which recorded over $600 in transactions in Q4 2020, are already exceeding that last year’s record. This flow of capital is primarily accruing to the benefit of the large MSOs. Yet, that creates the potential of alternative sources of funds from which smaller operators can benefit. Last year the SEC created a new ruling lifting methods of access to capital that have been hurdles to industries such as cannabis. And as more debt providers come online, debt as a capital source for cannabis operators becomes a more rational access to capital. Advisors experienced in the cannabis industry are a resource investors should first consider turning to when assessing incorporating these sources into their investment strategy.

How We Can Help

At Highway 33 Capital Advisory we excel at structuring deals to provide access to capital while meeting client investment strategies in emerging 2021 opportunities with our core expertise in Cannabis along with other highly regulated markets in the fields of Pharma, Biotech, Healthcare, Agtech, Clean/ClimateTech, and CBD/hemp companies. We specialize in thoroughly vetted companies looking to drive growth and enterprise valuations through M&A, non-dilutive debt financing and/or capital investments ranging from $5M to $100M+.

Let’s talk about putting the power of this expertise to work for you as a Sell-side or Buy-side client.