Investor Takeaway

The tide of capital flowing into the industry has risen substantially as investors become more confident in the results of state-by-state legalization and the positive signs of the federal de-scheduling progress. Capital raises have totaled $25.6 billion since 2019, while the first three quarters last year alone accounted for over $10 billion. This is happening in an industry growing at a CAGR since 2018 of 21%. Yet, stock performance of the pubcos continues to decline, operating expenses and supply chain disruption are on the rise, and we are entering an uncertain economic period. Why then is Business Insider running a headline that: “Top cannabis VCs predict a slew of M&A deals in 2022?” This week’s issue of the EDGE Briefing looks at the sources of capital opening to cannabis operators and ways investors can assess incorporating these sources into their strategic investment portfolio.

Capital Flowing Into the Industry

Even while investors await the beginnings of the de-scheduling process by the federal government, with what had been the expectation of the SAFE Act becoming law by now, capital continues to flow into the cannabis industry at a record pace. New Frontier Data reports in Cultivating Capital: Cannabis Finance & Investment, found that since 2019, capital raises in the cannabis industry have totaled $25.6 billion, with $10.1 billion in the first three quarters of 2021 alone. This is the case in an industry that i.lynchpinSEO.com found grew at around a 21% CAGR between 2018 and 2022. Insurance information resource HUBInternational.com reports record sales for the industry of $24 billion in 2021, with expected annual sales of $70 billion by 2028.

The law firm Reed Smith predicts even greener pastures for the industry in 2022 spurred on by the Green Wave of legalization washing over the Northeastern states, Virginia becoming the first in the South to legalize adult-use, and the fact that Arkansas, Florida, Idaho, Mississippi, Missouri, Nebraska, North Dakota, and Ohio all have cannabis-related initiatives on their 2022 ballots.

Yet, MarketWatch points out that the Cannabis ETF THCX is down about 15% so far in 2022, compared to a loss of 5.2% by the S&P 500 and a drop of about 10% by the Nasdaq composite during this same period in Q1.

With slack demand for their stock now, companies are often avoiding additional stock issuances that could dilute their share prices even more.

Additional hurdles to industry growth are reported by HUB International.

Insurance for cannabis businesses remains expensive. Cyber coverage is expected to rise 30% or more, as cyber risks explode and more businesses seek coverage. Executive liability policies including Employment Practices Liability (EPL) and Directors & Officers (D&O) premiums are expected to increase 10% to 20%.

HUB International goes on to confirm what we and most other industry watchers have been saying, that the biggest obstacle to cannabis industry growth is a lack of access to capital.

Access to Capital

So why then is the banner headline in Business Insider (BI) recently saying: “Top cannabis VCs predict a slew of M&A deals in 2022” – amid more cash and slow regulatory changes?

MJBizDaily reports figures that likely influenced the survey responders. They cite that New York-based Viridian Research counted 306 M&A transactions through mid-December last year, well above the 86 recorded for the same period in 2020. The ’21 total included 209 in the U.S., $10.1 billion in value, both of those numbers exceeding what was recorded in 2019 and 2020 combined.

The BI survey sees this trend set to continue throughout 2022.

That could mean huge amounts of consolidation for the space, which remains highly fragmented, as big players with financial backing gobble up smaller operators across the country. Consolidation could paint a clearer picture of the winners in an industry where it can be hard to tell which companies will succeed and which will fail.

This, once again, was the sentiment of the VC executives even if reform is not readily forthcoming at the federal level. In fact, with de-scheduling not likely to happen quickly, some venture capitalists told BI that slow regulatory changes at the federal level may also have a large hand in pushing companies to make deals in the space. For example, a reform bill called the SAFE Banking Act could help cannabis companies of all sizes access institutional investors – but despite large bipartisan support in the House of Representatives, the bill hasn’t passed the Senate. This keeps access to capital scarce, especially for smaller players.

In their interview with 14 VCs invested in cannabis the general sentiment was stated by Matt Hawkins, a managing…

Matt Hawkins, a managing partner at Entourage Effect Capital. He told BI that he thought the U.S. cannabis companies are positioned to scale and succeed whether or not federal reforms would attract further investments.

And HUB International is even informing its insurance audience that the additional risks and higher insurance premiums, quoted above, won’t inhibit industry growth. With large cannabis companies having an easier time accessing capital the result will be more M&A activity in 2022, as large cannabis businesses will have the means to acquire smaller competitors.

Capital Creation from M&A Transactions

As previously reported in The EDGE, capital creation through M&A will increase in 2022 due to what Technical 420, for one, states – that regardless of where federal de-scheduling stands, continued consolidation will be the norm in the cannabis industry. They cite the finding that the most recent M&A transactions have taken a more strategic and bolt-on approach to the due-diligence process. They see these three factors as characteristic of the growing maturity of the cannabis industry that these recent consolidations exemplify:

- Acquirers are looking for assets that are strategic and complementary in nature.

- The markets opening with a broader price range of acquisitions – from <$20 million to nearly $1 billion.

- A shift from acquisitions that leveraged market outside the U.S. to the many transactions now occurring that are leverage to the U.S. market.

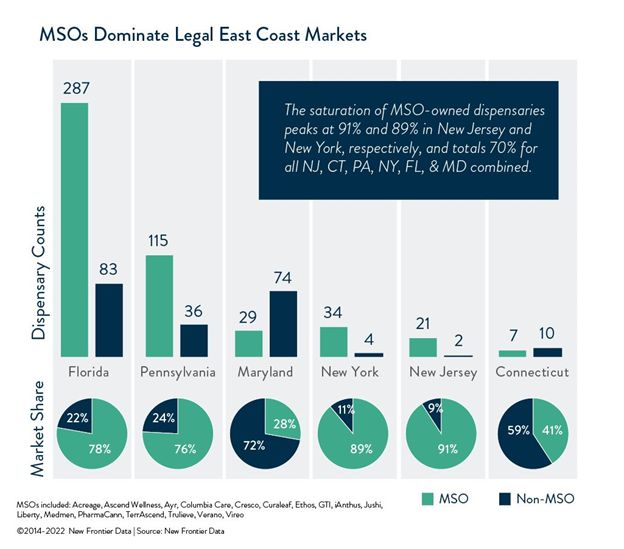

In fact, New Frontier Data shows that through M&A and aggressive statewide retail rollouts MSOs are gaining higher market share in the newer legal markets than in the established markets in the West.

Forbes sums up the key drivers propelling industry growth as regulations, marketing and scale. Inconsistent laws state-by-state and restrictive tax regulations limit the ability of an individual operator to scale. This choking effect on margins provides further impetus for consolidation in the industry.

SPACs in Cannabis

With many VC and PE investors, as well as most institutional investors, staying away from the industry, this puts the use of Special Purpose Acquisition Companies (SPACs) in the limelight – for cannabis companies in the U.S. and in Canada to access capital over traditional sources and in order to pursue the path of going public. SPACs, although showing mixed results in the cannabis industry to date, are an alternative that is bringing substantial liquidity to maintain sales growth and provide cannabis companies with the competitive advantage of more quickly getting to market. In many cases the SPAC merger process with a target company, termed a “de-SPAC,” can take place in a substantially shorter period of time than the traditional IPO timeline. This, though, must be accomplished in a relative short period of time – the two-year requirement for all funds to be invested or, if not, returned to investors.

Cannabis Industry Maturing to the Point of Turning to Debt

While the pace has slowed of late, debt issuance comprised 52% of trailing four-week capital raises as of Jan. 28, as reported by Viridian Research. This is up from <10% at the end of the year. Total capital raises in the first month of 2022 came in at about $249 million, down 81% from the year-ago period.

As more debt providers come online, recent multimillion-dollar debt funding among cannabis industry leaders shows that debt as a capital source for cannabis companies is a rational use of capital – potentially cleaning up balance sheets and enabling access to funding for expansion and/or the purchase of distressed assets coming out of the pandemic – to use debt financing for competitive advantage in the marketplace.

While the industry has been capital-constrained, borrowing against assets has been a key source available for many cannabis companies to pursue. Vertically integrated cannabis companies often have significant real estate and other assets that can be leveraged. What has changed now, though, is that more debt providers have come online over the past couple of years addressing a range of needs. Debt financing and the types most readily available to cannabis operators, including the alternative of the Medium Term Note (MTN), are described in greater detail relative to the SAFE Act in a recent issue of The EDGE.

The law firm, Reed Smith concludes that the rise of debt in cannabis has two primary drivers: the large asset base financed by capital raised in the public markets now used as loan collateral to fund growth, and the downside protection to investors by lending against assets as opposed to taking more risky equity positions.

Finding The Right Fit for Your Investment Strategy

What we have concluded is that 2022 offers an array of opportunities in M&A transactions, of all sizes, and of non-dilutive debt financing. What we advise our investors as they assess the market in which they see as the most advantageous boils down to this:

Finding the right fit for your strategic investment portfolio, or the correct way to appeal to a source for your growth funding comes down to clarifying the investment needs and objectives of all parties, determining the real value in the business by calculating a well-substantiated valuation, and matching the right investors with the right funding opportunity – the right operators whose objectives and scalability are a fit for investors’ portfolios.

How We Can Help

At Highway 33 Capital Advisory we excel at structuring deals to meet client investment strategies in emerging 2022 opportunities with our core expertise in Cannabis and other highly regulated markets in the fields of Pharma, Biotech, Healthcare, Agtech, Clean/ClimateTech, and CBD/hemp companies. We specialize in thoroughly vetted companies looking to drive growth and enterprise valuations through M&A, non-dilutive debt financing and/or capital investments.

Let’s talk about putting the power of this expertise to work for you as a Sell-side or Buy-side client.